Subscribe in a reader

Subscribe in a reader

Tuesday, February 19, 2013

RSS Subscribers

The old RSS feed for this website is no longer active. Please click the icon below to re-subscribe to the working RSS feed.

Subscribe in a reader

Subscribe in a reader

Friday, February 15, 2013

Moving on Up!

Avondale is moving! We are joining the stocktwits blog network to pair up with some of the best financial bloggers on the internet.

As a result, our blogspot address (avondaleassetmanagement.blogspot.com) will no longer be updated. Please visit us from now on at www.avondaleam.com

Tuesday, February 12, 2013

The Swiss National Bank's Currency Peg

Between the Yen and the Euro, the foreign exchange markets have seen some excitement in recent months. One currency cross that has been anything but exciting though has been that of the Euro against the Swiss Franc (EUR/CHF). After a rapid depreciation of the Euro during the heart of the European Financial Crisis, the Swiss National Bank decided to explicitly peg the Swiss Franc at 1.20 EUR/CHF. The SNB had maintained a "soft peg" up until that point by purchasing EUR in the open market, but the explicit peg was needed to stop the appreciation.

Below is a chart of the evolution of the SNB balance sheet as it has tried to stop the CHF from appreciating. The balance sheet has expanded by nearly 5x and foreign currency now represents almost 90% of the bank's assets. As a result, the CHF has effectively become backed by the Euro.

Below is a chart of the evolution of the SNB balance sheet as it has tried to stop the CHF from appreciating. The balance sheet has expanded by nearly 5x and foreign currency now represents almost 90% of the bank's assets. As a result, the CHF has effectively become backed by the Euro.

Monday, February 11, 2013

Where do Growth Stocks Peak?

Over the course of the recent bull market there have been a few growth stocks that have hit extreme levels only to come crashing down. Although some of these have recovered slightly, those that come to mind include: NFLX, GMCR, OPEN, MNST and CMG.

As a post-mortem on these stocks, below is a chart of the price to sales multiples that they hit at their highest levels. For comparison I included the peak price to sales multiples of five stocks that had similar sentiment (judged subjectively) at the 07 peak and five from the dot com era. Also included are the current multiples of six growth stocks that haven't slowed since 2009.

|

| Note: red bar is the average multiple for the group |

Total Fiscal and Monetary Stimulus Since 2008

As many are hopeful that we are finally leaving the financial crisis behind, sometime in the not too distant future the government is going to have to start unwinding the major stimulus that it has provided to the economy through fiscal deficits and monetary expansion since the crisis began.

Below is a cumulative tally of how much stimulus has come from the Fed and Treasury over the last four years. The total is now about $7T ($5T worth of deficits plus another $2T worth of monetary expansion). Amazingly, to the extent that one believes that the crisis was primarily housing market related, the $7T total represents ~70% of all the mortgage debt outstanding in 2008.

Below is a cumulative tally of how much stimulus has come from the Fed and Treasury over the last four years. The total is now about $7T ($5T worth of deficits plus another $2T worth of monetary expansion). Amazingly, to the extent that one believes that the crisis was primarily housing market related, the $7T total represents ~70% of all the mortgage debt outstanding in 2008.

|

| Cumulative deficit plus change in size of Fed balance sheet since 9/2008 |

Friday, February 8, 2013

Finance Website Web Traffic Comparison

Below is a comparison of the web traffic rank of some of the most popular finance sites on the web. The list was formulated simply based on websites that came to mind, so it's highly probable that I missed some high traffic sites in here somewhere. CNN money, yahoo finance and google finance are also three big finance sites that would make the list which can't be extracted from their larger parent sites.

For all the fragmentation of news that the web has caused, the big guys still get the most traffic. Business insider is the lone new-media entrant which has competitive traffic numbers to Forbes, etc. The only true blog that makes this list is zerohedge. The average big name finance blog has a rank between 20,000 and 200,000.

For all the fragmentation of news that the web has caused, the big guys still get the most traffic. Business insider is the lone new-media entrant which has competitive traffic numbers to Forbes, etc. The only true blog that makes this list is zerohedge. The average big name finance blog has a rank between 20,000 and 200,000.

|

Thursday, February 7, 2013

Monetary Base Breaks Out

Data released by the Fed today confirmed that the Monetary Base has officially risen above the range that it had settled in since July of 2011. Since roughly the same time period brent crude oil and gold have also been stuck in a prolonged sideways move, although in recent weeks crude has also begun to turn higher along with the base.

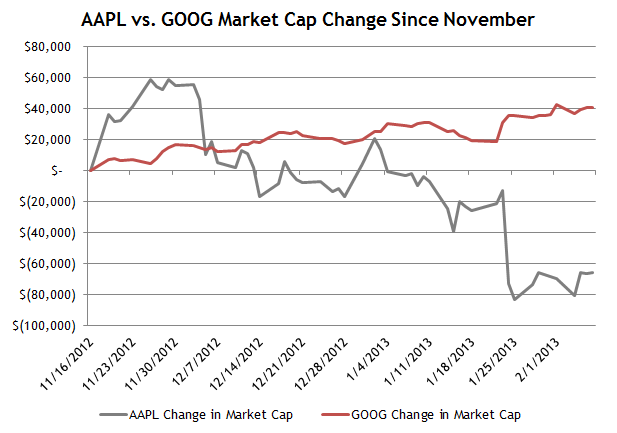

Is AAPL's Loss GOOG's Gain?

Although GOOG refuses to directly monetize its dominant position in mobile, one might expect that any lost market cap for AAPL might be gobbled up by GOOG because the two are an effective duopoly in smartphone operating systems. Below is a chart of the change in market cap for AAPL and GOOG since November 16. Since then GOOG has gained $40B in market cap as AAPL has lost $65B.

Note: I chose to start the chart on November 16 rather than AAPL's September high because that's when the S&P 500 bottomed after a 5% pullback. I reasoned that this time period was less influenced by beta.

Nikkei Long Term Chart

In concert with the Yen's 20% depreciation since October, the Nikkei has rallied 35% over the same time period. It's a large move to be certain, but, also like the Yen, in the context of the index's long term chart, it is almost inconsequential. Below is a chart of the Nikkei since 1984. The index is still 70% below its all time peak set in 1989 and 35% below it's 2007 peak. Of course, if one were to price the index in dollars the picture would be slightly altered, but the value destruction is inescapable.

Wednesday, February 6, 2013

February 2013 Investor Letter

Below is a letter that is written monthly for the benefit of Avondale Asset Management's clients. It is reproduced here for informational purposes for the readers of this blog.

Dear Investors,

So far 2013 has unfolded mostly in line with the expectations voiced in last month’s letter. Valuation, stimulus and sentiment have combined to give the market a generous boost to start the year. The S&P 500 was up 5% in January which, like last year, was the best January since 1997.

In last year’s February letter I pointed out that a good January has historically been a good sign for the rest of the year: “Since 1957 there have been 18 times that the S&P 500 was up 4% or more in January. In those 18 years, the S&P was up an average of 21%, and returned double digits for the full year 17 out of 18 times.” I wrote then that these statistics were encouraging, but that a high single digit to low double digit return was more likely for 2012. This year I am inclined to believe that the S&P 500 could be up 20% at some point mid-year, but it would be surprising to me if it held on to close the year at that level.

It is worth noting that the Dow, which has a longer history than the S&P 500, also shows strong returns in years with a large gain in January. However, 1914, 1929 and 1987 were also all years with big gains in the first month. These years have the unfortunate distinction of being ones in which the Dow had its three worst days in history, all of which came in the last few months of the year. That’s not to say a crash is likely, but it is something to keep in mind should markets become over-extended as the year goes on.

For now, investors aren't spending much time thinking about negative scenarios. As the year started, people were still gloomy about the prospects for 2013, but one month into the year the mood has gotten much more optimistic much faster than I expected. Signs of optimism are numerous: flows into equity funds were the largest in a decade, negative economic reports have had little effect on the market, the Euro has recovered back to €/$1.35, and even the US Congress is getting the benefit of the doubt. After years of constant crisis people seem ready to take risks again, including CEO's, who have been very upbeat on recent conference calls.

When investors become this bullish, it means that it’s important to act cautiously. Rapidly rising prices are warning signs that price insensitive investors have entered the markets. They bring with them the opportunity to sell at higher than reasonable prices, but also introduce added volatility.

This is an uncomfortable circumstance for investors who are price sensitive, but it’s not yet time to sound the alarms for two principal reasons. 1) Valuation is becoming stretched but not necessarily extreme. My work at the individual stock level suggests that the average stock could rise another 20% before valuation makes no logical sense. 2) I suspect that most of the new found bulls are really bears in bull clothing ready to turn on the market at a moment’s notice. We’re not quite at the level where there is unanimous belief in the bull, which is typically the final phase of a bull market.

Still, such positive sentiment does increase the chances that there could be short term pullbacks over the next few weeks and months. Markets never rise in a straight line and so mild corrections are within normal expectations. Absent unique opportunities, we are unlikely to be large buyers of stocks for the time being. We continue to be happy to sell at the right prices.

Scott Krisiloff, CFA

Dear Investors,

So far 2013 has unfolded mostly in line with the expectations voiced in last month’s letter. Valuation, stimulus and sentiment have combined to give the market a generous boost to start the year. The S&P 500 was up 5% in January which, like last year, was the best January since 1997.

In last year’s February letter I pointed out that a good January has historically been a good sign for the rest of the year: “Since 1957 there have been 18 times that the S&P 500 was up 4% or more in January. In those 18 years, the S&P was up an average of 21%, and returned double digits for the full year 17 out of 18 times.” I wrote then that these statistics were encouraging, but that a high single digit to low double digit return was more likely for 2012. This year I am inclined to believe that the S&P 500 could be up 20% at some point mid-year, but it would be surprising to me if it held on to close the year at that level.

It is worth noting that the Dow, which has a longer history than the S&P 500, also shows strong returns in years with a large gain in January. However, 1914, 1929 and 1987 were also all years with big gains in the first month. These years have the unfortunate distinction of being ones in which the Dow had its three worst days in history, all of which came in the last few months of the year. That’s not to say a crash is likely, but it is something to keep in mind should markets become over-extended as the year goes on.

For now, investors aren't spending much time thinking about negative scenarios. As the year started, people were still gloomy about the prospects for 2013, but one month into the year the mood has gotten much more optimistic much faster than I expected. Signs of optimism are numerous: flows into equity funds were the largest in a decade, negative economic reports have had little effect on the market, the Euro has recovered back to €/$1.35, and even the US Congress is getting the benefit of the doubt. After years of constant crisis people seem ready to take risks again, including CEO's, who have been very upbeat on recent conference calls.

When investors become this bullish, it means that it’s important to act cautiously. Rapidly rising prices are warning signs that price insensitive investors have entered the markets. They bring with them the opportunity to sell at higher than reasonable prices, but also introduce added volatility.

This is an uncomfortable circumstance for investors who are price sensitive, but it’s not yet time to sound the alarms for two principal reasons. 1) Valuation is becoming stretched but not necessarily extreme. My work at the individual stock level suggests that the average stock could rise another 20% before valuation makes no logical sense. 2) I suspect that most of the new found bulls are really bears in bull clothing ready to turn on the market at a moment’s notice. We’re not quite at the level where there is unanimous belief in the bull, which is typically the final phase of a bull market.

Still, such positive sentiment does increase the chances that there could be short term pullbacks over the next few weeks and months. Markets never rise in a straight line and so mild corrections are within normal expectations. Absent unique opportunities, we are unlikely to be large buyers of stocks for the time being. We continue to be happy to sell at the right prices.

Scott Krisiloff, CFA

Opinions voiced in the letter should not be viewed as a recommendation of any specific investment. Past performance is not a guarantee or reliable indicator of future results. Investing is subject to risk including loss of principal. Investors should consider the suitability of any investment strategy within the context of their personal portfolio.

CPI Adjusted S&P 500

As the S&P 500 continues to approach its former all time high, below is a long term chart of the index adjusted for CPI. While we're not too far from the 2007 highs on a nominal basis, the index is still about 11% lower than it was in 2007 on a CPI adjusted basis and 25% lower than the all time high reached in 2000. The armchair technician in me has drawn a line to point out that we're approaching inflation adjusted resistance.

US Post Office Volumes

The USPS made news today by announcing that it would stop delivering mail on Saturdays. The postmaster general made an interesting comment on CNBC this morning that part of the problem is that the cost of postage can't be raised by more than the rate of inflation. Still, it's tough to maintain profitability in any business when volumes look like the chart below. Since 2000 the number of first class letters handled by the USPS has fallen by 33% to 68 billion. I wonder how much of what's left is junk mail...

I hadn't realized this before, but the post office actually files a 10-K which can be found here. Below is the income statement pulled from the filing.

I hadn't realized this before, but the post office actually files a 10-K which can be found here. Below is the income statement pulled from the filing.

Tuesday, February 5, 2013

Is the Yen Crashing?

Considering the magnitude of the move, the Yen's recent depreciation vs. the dollar has garnered surprisingly little attention. Since September the Yen has gone from USD/JPY 77 to 93. That's a 20% decline from peak to trough, which is a relatively extreme move for a currency. Below is a rolling three month change chart for the Yen going back to 1971. This is the 2nd largest three month move for the Yen in that time frame.

By comparison, the largest 3 month decline for EUR/USD was 20% in 2008 under the stress of the financial crisis. During the heart of the European financial crisis in 2010/2011, as the world worried that the Eurozone would collapse, the most that the currency depreciated versus the dollar was 13% in a three month period.

McGraw Hill Market Cap Decline

Efficient market theorists should take note that MHP's market cap has fallen by $3B in the last two days on news that the Federal government is suing the company. For reference BP's settlement with the Justice Department was $4B. Given that McGraw Hill was arguably complicit but not the direct cause of structured credit blowups, it's difficult to see how any settlement could reach multi-billion dollar territory.

Monday, February 4, 2013

Sector SPDR Snapshot

Below is a snapshot of how the Sector SPDR ETFs have performed since 2003. As the S&P 500 approaches its 2007 high (perhaps not today) four of the sectors have already made new all time highs. Consumer Staples (XLP), Healthcare (XLV), Consumer Discretionary (XLY) and Tech (XLK) have powered much of this bull market, although Tech (XLK) has not made it past its September high. Thanks to the dilution in the financial sector it may be a very long time before XLF reaches its former peak.

|

| Click to Enlarge |

Friday, February 1, 2013

Cities With Multiple Pro Sports Champions in the Same Year

No market analysis here, but thought it would be interesting to point out that if the 49ers win on Sunday it will be the 14th time in history that a city holds two pro sports championships at the same time. Below are the other 13 times that it's happened.

Since the Super Bowl only started in 1967 the years in red are the multi-championship years that hold up in the modern era. While I'm at it, I should probably put an asterisk next to 2002 as well though. The Angels are from Anaheim, not Los Angeles.

|

| Source: Wikipedia |

S&P Annual Performance After a Big January

This is an update to a post that I first wrote last year, the last time that the S&P 500 had a big rise in the first month of the year.

When the S&P 500 has a good first month, it has statistically been followed by a really good year. The index has risen by more than 4% in January 18 times in its 56 year history. In those years it has averaged a 21.1% return for the full year, and it has been up double digits in every one of those years except for 1987 (which was a good year up until the October crash).

The S&P 500 has never been negative in a year with a big January, but it's worth noting that if a similar analysis is performed on the Dow, which has a 118 year history, there are five years (out of 28) that the index was up more than 4% in January and ended negative for the year. Many of those years were significantly negative too: the average loss was 18.4% and the list includes 1914, 1929 and 1930. The index ended those years down 30.7%, 17.2% and 33.8% after being up 5.1%, 5.8% and 7.5% in January respectively.

Weird eerie coincidence, the Dow has had a daily crash three times in its history: in 1914, 1929 and 1987. All three years had big Januaries.

When the S&P 500 has a good first month, it has statistically been followed by a really good year. The index has risen by more than 4% in January 18 times in its 56 year history. In those years it has averaged a 21.1% return for the full year, and it has been up double digits in every one of those years except for 1987 (which was a good year up until the October crash).

The S&P 500 has never been negative in a year with a big January, but it's worth noting that if a similar analysis is performed on the Dow, which has a 118 year history, there are five years (out of 28) that the index was up more than 4% in January and ended negative for the year. Many of those years were significantly negative too: the average loss was 18.4% and the list includes 1914, 1929 and 1930. The index ended those years down 30.7%, 17.2% and 33.8% after being up 5.1%, 5.8% and 7.5% in January respectively.

Weird eerie coincidence, the Dow has had a daily crash three times in its history: in 1914, 1929 and 1987. All three years had big Januaries.

Thursday, January 31, 2013

Earnings Call Notes 1.31.13

Below are quotes from an assortment of recent earnings calls--snippets of information that I find relevant (typically on a macro/industry level) from companies that I have some working understanding of. Complete transcripts can be found at Seeking Alpha.

Banco Santander (SAN)

Facebook (FB)

Banco Santander (SAN)

capital ratios rising for the sixth year running up to 10.33%. loan-to-deposit ratio is now below 100%Southern Company (SO)

we have assigned since the beginning of the crisis over EUR 23 billion to specific provisions for loan losses and real estate, which account for 10% of our total loan portfolio in Spain.

As for our NPL ratios, the group ratio was 4.54%

And if we look at lending, lending fell overall by 6%, but big differences between segments. real estate purpose fell 32%; the individual household mortgages and consumer loans down 7% due to household deleveraging...reasonably stable lending to companies and to the public sector...balances with large corporates have fallen, too...because of continued deleveraging by corporates.

Brazil, the macroeconomic environment has been quite different to what we expected and what the market expected...Growth on GDP was of about 1%....we think that is going to pick up in 2013 and grow at about 3%. Interest rate at historic growth, 7.25% and inflation almost 6%.

In Spain, the recapitalization of banks and the private sector adjustment already completed

In short, we believe that the worst part of the cycle is already over. Realistic exposure is fully provisioned.

Whether we plan to repay anymore or return anymore [of the LTRO], we are using as cushion basically or insurance...So the decision of whether to repay any more or return any more, well, the answer would be probably, yes. But it will depend on the evolution of the markets and the impact on our income statement, well, it costs 75 basis points...And the liquidity buffer had a negative impact on our income statement

We continued the ongoing transformation in our generation mix, generating more energy from natural gas than coal for the first time in our historyDow Chemical (DOW)

our kind of color on where we believe the economy is headed is slightly more bullish than we were, say, in the third quarter. We are expecting a backend loaded economic recovery but I feel pretty good about it right now based on what we see.

energy efficiency has almost no influence on the consumption of our customers. 88% or so of usage can be explained by either the income growth of our customers, the price of our product and weather.

We all have these goofy devices. We all have iPads and iPhones and bigger plasma TVs and everything else and when we see the progression that people are moving from small homes to apartments into you now primary housing, we see a growth in square footage per person...All of these things contribute to usage growth

if the final rule is anything like the proposed rule, conventional coal generation is just not doable...I go back to the families we serve, 48% of which make 40,000 or less, those folks make tough kitchen-table economic decisions every day. Their demand for energy is relatively inelastic, and so anything the EPA does which adds cost to energy tends to slow down our economic recovery

wet shale gas dynamics are fundamentally changing the game for integrated North American based producers like Dow. This is clearly evidenced by operating rates in the United States and Canada being in the 90s, while Asia and Europe have been in the 70s.Time Warner Cable (TWC)

as global demand outstrips supply in the next few years and world GDP gains further traction, we anticipate operating rates higher than 90% leading to substantial margin expansion, a double peak, so to speak.

Dow's feedstock flexibility will allow us to continue to pivot so that we continue to take advantage of our uniquely advantaged feedstock slate and we are building on this advantage.

Our programming costs per subscriber has grown 32% in the last 4 yearsQualcomm (QCOM)

Our residential video ARPU increased 16% over that same period, so we've effectively raised pricing a little faster than inflation but only half as fast as programming costs have risen.

ARPU per customer relationship, which increased 4% over last year and is approaching $120 per month

We do not pretend that these deals [i.e. the Dodger's deal] are inexpensive or cheap. And our sense is that if we're going to carry these games, they're going to be expensive when we get them. So what we think we've done with these deals is to minimize and stabilize the cost over a long time period.

On Google in Kansas City: The reality is, today, there are not really applications that require 1 gigabit per second.

this brings 3G penetration to 29% in China, so excellent progress and still plenty of opportunity aheadUPS (UPS)

our design pipeline continues to grow. There have been more than 600 Snapdragon-based devices announced and another 170 plus devices announced based on our Qualcomm Reference Design solutions.

we are seeing more efficiency in the 3G, 4G inventory channel as the industry continued to move toward an open retail channel versus a carrier centric channel

We are reaffirming our estimate for calendar 2013 3G, 4G device shipments of between 1 billion and 1.07 billion units, up approximately 8% to 15% year-over-year

in the U.S, we were off to a surprisingly strong start in January

Holiday retail sales came in slightly below expectations but UPS still hit a new high, delivering over 500 million packages globally during peak season.

On our peak air day, Christmas eve, UPS delivered over 8 million air packages, more than 2.5 times our normal air volume and over 1 million pieces more than last year.

UPS annual revenue of $54.1 billion was our highest ever, as were the 4.1 billion packages we delivered globally.

I think that overall we still see 2013 as a slow growth economy.

Facebook (FB)

We started off the year with no ads at all on mobile and we ended up with approximately 23% of our ads revenue coming from mobile in the fourth quarter.Paccar (PCAR)

Marketers are realizing more and more that Facebook is one of the best places to reach their customers on mobile because of our unique ability to reach specific target audiences at scale.

our total expenses, excluding stock comp, will likely grow by somewhere around 50% in 2013

PACCAR's retail share of the U.S. and Canadian Class 8 truck market was 28.9% and DAF's share of the European above 16-tonne market was 16%Core Labs (CLB)

Looking at the truck market overall in 2013. The U.S. and Canadian Class 8 industry retail sales are estimated to be in the range of 210,000 to 240,000 units. In Europe, the "greater than 16 tonne" truck market is anticipated to be in the range of 210,000 to 250,000 units.

Natural gas will be a factor, but at this time it's a pretty small factor. We'll just have to see over time how the infrastructure shakes out

Yeah, Jeff, we actually don't think that the shale plays are well understood at this point. Just over the last couple of quarters, we have been able to determine through our fracture diagnostics technology that additional stages, closer spaced, so you have more in greater contact with the reservoir phase is going to proliferate more stages and more closely space stages.

We believe that currently there are only one or two countries that have spare capacity and that amount is fairly limited. If we get some robust economic growth around the world, we are going to see crude prices, Brent prices right back at $150.

Q: perhaps two substantial liquids discoveries yet to be made or announced in North America, can you give us a feel for when we might, the mystery might go way? A: Well, that’s up to our clients, acreage positions are being taken and I got a fairly, once of the acreage positions are established as which happened in the Eagle Ford and then in the Utica announcements will be made. So it’s not up to us, its up to our clients.

Conoco Phillips (COP)

Viacom (VIA)We ended 2012 with just over 8.6 billion BOE of reserves, up 3% overall compared to 2011. Importantly, we added 942 million net BOE of reserves organically resulting in an organic reserve replacement rate of 156%

I think as we look out and think about the future opportunity, I think with this unconventional revolution that we are seeing in North America right now, and some of the technology advances in the deepwater arenas that are becoming pretty perspective. It’s kind of in my view turn from a bid of resource scarcity that was leading to a lot of merger synergies over the last 10 or 12 years and resource capture into a view now...we just think that growing organically, there is the opportunity set to go do that and the option value associated with growing organically is, we thought better in our portfolio then trying to do that through an M&A channel, or some resource access that way.

the consistent refrain we hear from our audiences is that they want new shows and new episodes in faster cycles, and so we are delivering at all our networks, accelerating development timelines and production to accelerate our ratings turnaround.Under Armour (UA)

original programming that’s new and exclusive to us where we own all the rights and we think that is going to be critical as you move into the future where this program lives across platforms and around the world.

we have content on platforms like Netflix and Google. The growth of streams of our content far outpaces the growth of subscribers that they have

In our IPO year of 2005, compression represented 64% of our apparel mix. This past year, that compression number was down to just 14%.Cullen/Frost Bankers (CFR)

we want to go back to this concept around cluster marketing, and the idea there is to create holidays. So holidays are places where based on the entire brand meets at once. What we want to do is consolidate our spend to tighter, but louder messaging

For the year, return on average assets and equity were 1.14% and 10.03%...average total deposits were $17.3 billion, up 13.6%...average loans were up 11.2%Bank of Hawaii (BOH)

It’s really nice when you’re growing this strong organically. Just to put it in perspective, the biggest bank we ever bought was about a $1 billion. And today, we’re growing at a rate of about $2 billion a year. So this organic is getting better.

You don’t just go make the first call and get the loan...We know that the work we do today is going to payoff about a 120 days from now.

you’ll see a juvenile delinquent come in [to our markets] every now and then, and that juvenile delinquent doesn’t mean a little bank. It means, usually the too-big-to-fail will come flying in with some crazy pricing.

We had a record number of visitors to Hawaii this year and visitor spending reached a record-high of 14.3 billion that's up over 18% for the year. most of that increase coming from our International segment.

Year-to-date return on assets was 1.22% and return on equity was 16.2%. Our year-to-date efficacy ratio was 57.9%, a reduction from 59.2% in 2011. Earnings per share was up 8.3% in 2012. Loans grew 5.7%. Shareholders equity grew 1.9%.Callaway (ELY)

From a market share basis, through November our US hard goods market share declined to 14.4% versus 15.6% in 2011Hershey (HSY)

what’s occurred between 2007/2008 and the current somewhat compressed gross margins is rising costs out of Asia where we source most of our products, and an increase in the amount of technology in the products such as adjustable drivers and other technologies that in many instances are being sold at the same price points that we’re popular in the market in 2007/2008. So those factors are real in our industry as candidly they are in all industries, and we have to work through those.

Halloween results were in line with expectations. The late October storm that affected the East Coast did not have a material impact on our overall Halloween results.

Oil Priced in Yen vs. Dollars

The USD/JPY exchange rate has risen to ¥91 from ¥77 as Japan seems intent on creating inflation for itself by depreciating its currency. Thanks to that depreciation oil priced in yen is rising even as it is relatively flat when priced in dollars. Success?

|

| Brent crude price |

Wednesday, January 30, 2013

Earnings Call Notes 1.30.13

Below are quotes from an assortment of recent earnings calls--snippets of information that I find relevant (typically on a macro/industry level) from companies that I have some working understanding of. Complete transcripts can be found at Seeking Alpha.

Amazon (AMZN)

There is not a lot I can comment on in terms of our plans similar to last year no as we progress through the year, we can give you further updates on what we plan to do there....

there's not a lot more I can add to it...

just stay tuned and we will let you know as the year progresses...

we will continue to expand our footprint over time ...Beyond that there is not a lot I can add...

we haven’t given a lot of detail but I think one thing certainly to look at...

I can't give you specific numbers but we have seen very good progress...

I can't give you specific for attach rates but the business is making good progress...

I do not have a specific number for you there, but yes...

We will continue to add selection on the Instant Video. Beyond that, you have to stay tuned...

There are not a lot of specifics. We have long been in the practice of not talking about trends in within the quarter in terms of year-over-year growth or anything like that...

we haven't broken out the first-party versus third-party units since it's something we have done for that's only I am today or we have done in previous calls, so it's not I can help you with there...

There's not a lot I can specifically talk about as it relates to LivingSocial ...

Boeing (BA)

commercial airplane deliveries was 601 delivered, the most since 1999, and the second-most in commercial aviation history.

we also led the industry in net new orders, with 1,203, the second highest total in our company’s history

Our commercial backlog of nearly 4,400 airplanes totals a record $319 billion

Nearly two-thirds of our order book is with customers outside the U.S. and Europe

For the quarter, we delivered 23 787s, reaching a total of 46 for the year

doubling 787 production, increasing the rate from two airplanes per month to five per month

final assembly build rate to seven per month in mid 2013 and 10 per month by late 2013

The 737 production rate will increase to 38 per month in the second quarter of this year and then move up to 42 per month in the first half of 2014.

Jones Lang LaSalle (JLL)

while capital values continue to increase in most major markets around the world compared to the prior year, the rate of growth has slowed in a number of key markets.

The vacancy rates across 98 global markets remain stable in the fourth quarter at 13.2% as vacancy declines in the U.S. and Europe were offset by increases in Asia Pacific. Prime rental growth slowed in the quarter, increasing 2.1% year-on-year, while Beijing, Sao Paulo, Mexico City and San Francisco recorded the strongest rental growth in 2012 while demand falls, so prime rent decreased furthest in Hong Kong, Singapore, Paris, Madrid and Brussels.

institutional investors are maintaining and, in many cases, increasing their allocations to real estate, attracted by returns that compare favorably to other investment options.

Robert Half (RHI)

W.R. Berkeley (WRB)Small and midsize companies are hiring.

There is ongoing demand for flexible staffing. The percentage of temporary jobs created in the U.S. in this cycle is double that of the prior one, 13.2% versus 6.5%. The pace of temporary staffing growth in the current recovery also has been faster. 792,000 temporary jobs were created in the 39 months ended December 2012. In the prior recovery, it took 56 months to add 513,000 temporary jobs.

As of the end of 2012, the temp penetration rate in the United States was 1.9%, of total U.S. non-farm employment, which is close to the high point in the last cycle. This percentage is approaching the record high of just over 2% in 2000. There is opportunity, we believe, for the temp penetration rate to expand further based on the secular demand for staffing flexibility we have been discussing.

Affordable care act: we can legally help [our clients] remain under 50 [employees] since we're the employer of record for the temporaries we provide to them

It's estimated that there are 130,000 firms with 50 or fewer employees, that over half of them do not provide coverage to their employees.

the data would show that our European operations are bottoming

there would appear to be an increasing awareness of the impact that diminishing investment income is having on the industry’s economic model. While this macro situation is widely discussed, the sense of urgency in tackling these issues seems to vary from carrier to carrier. Having said this, there is an ever-growing percentage of the market that is pursuing rate in an effort to remedy the situation.Ford (F)

On Sandy: the industry received a wake-up call with regards to the imperfections of both cat modeling, as well as local building codes as we endure the impact that a large tropical storm can have on a region.

Workers’ compensation remains one of the lines of business where the market is most aggressive in seeking rate.

The excess casualty market is also showing early signs of a return to underwriting discipline

combined of a 98.1%. However, when one adjusts for storms as well as reserve development, we believe the company is running at about a 96.5%

With every passing quarter, it is becoming more apparent we are entering a hard market. The number of carriers seeking broad rate increases continues to grow, and the minority of companies that continue to act irresponsibly is a dwindling population. While it is true we have not yet reached the point where there is low-hanging fruit, it has been many years since we as an organization have been so encouraged by the market.

The benefits of start-ups are twofold. One, as opposed to buying something, you don’t get someone else’s problems. And two, you don’t get intangible assets on your balance sheet, you get to tax deduct the expenses of building the business, and you don’t have carry forward issues as you go forward.

In the fourth quarter, total company production was about 1.5 million units, 125,000 units higher than a year ago. This is 13,000 units higher than our guidance. We expect total company first quarter production to be about 1.6 million units, up 160,000 units from a year ago reflecting higher volume in all regions except Europe. Compared with fourth quarter, first quarter production is up 72,000 units.

This was our first U.S public debt issuance in about a decade and took advantage of favorable market conditions to issue low cost, long term debt.

Europe inventory destocking: It’s principally behind us. We still have a little bit of an imbalance...But the majority, the vast majority of the destocking is behind us.

Manpower (MAN)

Potlatch (PCH)Revenue in Southern Europe was slightly weaker than expected...Revenue in Italy was down 8%...Spanish market continues to remain soft in the quarter...higher vacation and lower bench utilization in Germany and Sweden, which also negatively impacted the gross margins...We continue to see soft demand within the Swedish market...Japan experienced modest growth...Australia continues to languish...Our business in China and India continue to grow nicely and contribute to the bottom line

Secular trends in the area of Manpower, Experis, Right, Manpower Group Solutions, and emerging markets are all there. In many cases, the voice of these positive secular trends have been ground out by the cyclical nature of what is occurring, particularly in Europe, but it cannot be underestimated.

The conversations we’re having with our clients and prospects for the need for agility is translating to much more of an outcome based solutions environment as well as the use of temporary staff to create the agility that is required

Our Wood Products division continues to perform exceptionally well bolstered by a significantly higher demand and pricing as the housing market recovers. Furthermore, the division finished the year with its best annual performance in the nearly a decade.ACE (ACE)

Like we are currently running our facilities at about 104% of capacity due to the amount of over time that we operate the facilities and that’s on a two shift basis.

The x cat [excluding catastrophe] accident year combined ratio was 91.4%

Book value per share grew about 2%, and our operating ROE for the quarter was 8%

Our commercial P&C business in the U.S. continued to benefit in the quarter from an improving price environment where we are now achieving rate-on-rate increases for the second quarter in a row, and I firmly expect this to continue.

From what I see today, I am more bullish about the pricing environment in the U.S. than I have been for some time.AK Steel (AKS)

Steelmaking input costs, namely coal, coke and iron ore, have fallen, and that will result in significant cost savings for us in 2013. Second, we expect to benefit from increased shipments to both the contract and spot markets in 2013 due to slightly improved overall demand and a greater share of the automotive market.Nucor (NUE)

New CEO John Ferriola: As we announced on November 16, I became Nucor's CEO at the start of this year.

current capacity utilization of just 75% for the U.S. steel industry.Waddell and Reed (WDR)

Nucor will continue to be proactive in bringing attention to the critical need for our government to enforce rules-based free trade.

Average productivity per advisor continue to increase reaching $44.3 thousand during the quarter, a record’s high.

We’ve seen a significant increase in the appetite for our equity products and we have not seen a concurrent diminution of the appetite for the fixed income products that had been working, which is to say, the sales are broad based and in that sense encouraging.J&J Snack Foods (JJSF)

Churros sales were up 33%...Soft pretzels sales however were up 5%...ICEE and frozen beverages, frozen beverage and related product sales were up 4%

Number of Days Since Last 3% Down Day

2012 was a pretty mild year as far as volatility is concerned. There were two periods of correction, but both were relatively light and there wasn't a single day that the S&P 500 was down 3% or more.

Markets have calmed down to the extent that it's actually been 448 days since the last time that the S&P 500 has fallen by 3% or more in a single day. At today's level on the Dow that would be a 400 point decline. For comparison, since 2008 we had grown accustomed to getting a decline that large once every 32 days on average.

Looking at S&P history since 1957, the current 448 day streak is better than average, but not quite at the best levels that the index has ever seen. Over that period, a 3%+ daily decline happens about once every 217 days. However there are several long periods without them. There was no such decline for 11 years between 1962-1973. Even recently there wasn't a 3% decline for nearly 1500 days between 2003-2007. That streak was broken on February 27, 2007.

Does Negative GDP Growth Portend Recession?

While it was generally expected that 4Q was a slow quarter for economic growth, it was probably a surprise to many that the growth rate was negative. What are the odds that this negative growth portends a recession?

Assuming that the revised number remains negative this is the 42nd time in 279 quarters since 1947 that quarterly GDP growth has been negative. Of those 42 times, 27 of them came during a recession (as defined by NBER). Therefore GDP has contracted 15 times while the economy was not in recession. Below is a list of those times. The economy entered into a recession in the following quarter five out of those fifteen times.

Of course, NBER defines recession dates after the fact, so we could be in a recession right now and just not know it. Given that the market is hardly lower today, that would probably be a surprising result.

Assuming that the revised number remains negative this is the 42nd time in 279 quarters since 1947 that quarterly GDP growth has been negative. Of those 42 times, 27 of them came during a recession (as defined by NBER). Therefore GDP has contracted 15 times while the economy was not in recession. Below is a list of those times. The economy entered into a recession in the following quarter five out of those fifteen times.

Of course, NBER defines recession dates after the fact, so we could be in a recession right now and just not know it. Given that the market is hardly lower today, that would probably be a surprising result.

|

| Note: Figures are NON-Annualized |

Tuesday, January 29, 2013

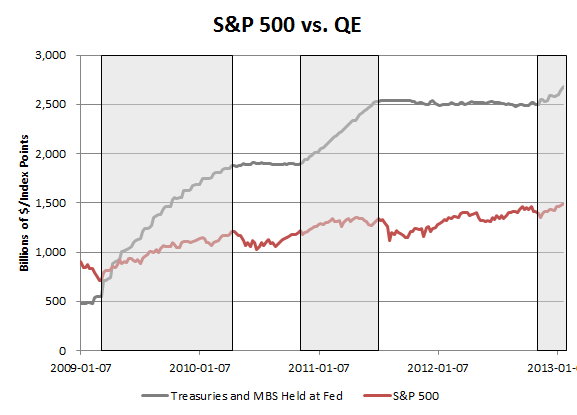

QE Effect on S&P 500

After QE3's announcement in mid September there was some concern that the effect of QE on the market had eroded because the S&P 500 proceeded to sell off by 5%. It could be true that QE is losing its efficacy, but it's worth noting that true balance sheet expansion didn't really start until mid November because of the mechanics of MBS purchases. It therefore may or may not be coincidental that MBS started to show up on the Fed's balance sheet around the same time that the S&P 500 found a bottom.

Below is a chart of how the S&P 500 has done during periods of QE, but instead of using the announcement dates, the chart highlights the times that the Fed's holdings of Treasuries and MBS were increasing (note that this analysis therefore excludes operation twist). Since the S&P 500 is now hitting new cycle highs, perhaps one could argue that QE hasn't exactly lost its potency.

Earnings Call Notes 1.29.13

Below are quotes from calls that I've read today--snippets of information that I find relevant (typically on a macro/industry level) from companies that I have some working understanding of. Complete transcripts can be found at Seeking Alpha.

Caterpillar (CAT)

"After a great first half the economies around the world began to slow around mid-year, and as a result dealer sales to end users began to flatten out. We found ourselves with inventory that was too high and dealers also found themselves with too much inventory. As a result dealers slowed orders, and in the third quarter we began the process of scaling back production. Now while production declined somewhat in the third quarter, we took it down much more in the fourth quarter, and because of that we were able to reduce inventory in the fourth quarter. "

"We've already seen pretty substantial pickup in construction orders in the fourth quarter. "

"On mining again, we had massive orders, I mean very large orders in mining throughout much of a ’11 and really through almost the entire first half of ’12. That’s when sentiment changed I think in the world economy it was evident, in China it was softer, you had an easing of commodity demand, although, overall mining activity actually did go up in ’12. So, orders on hand were quite significant and over the past six months customers have really eased off on ordering."Plum Creek Timber (PCL)

"Lumber and wood panel prices have increased significantly, encouraging lumber mills to increase their output. "

"Mill operators are reinvesting in their mills and some are adding shifts."

"contractor availability is expected to be a meaningful supply constraint to the industry"

"Southern sawmill owners are running extra hours to increase production to meet demand, and many are at the point where they are contemplating adding employees and an additional shift to meet the expected demand growth this year."

"assumptions that we'll see, 950,000 to 1 million housing starts next year, and we believe for that demand to be met, you're going to have to see an increase in production U.S. South, and the Southern production right now is about 14 billion board feet, and we expect that you'll see an increase in production in North America of about 3 billion board feet, and about half of it should come from the U.S. South."Harley Davidson (HOG)

"The biggest thing, I think, surprise in 2012 was just how low the retail credit losses were. At 79 basis points, clearly, the lowest we've seen in over a decade and considerably better than what we had seen in 2011."

"we think as far as the consumer is concerned, that they're starting to shift their behavior a little bit. We may see a little bit higher credit losses. "

"we said, I think, 3 years ago, that we were going to open between 100 and 150 new dealers around the world. As you mentioned, we're certainly on plan to do that. We believe that there is still opportunity really in every market."Yahoo (YHOO)

"talent is fundamental to our success. Attracting the best people to Yahoo! is critical, and we embarked on a number of initiatives to make Yahoo! the absolute best place to work."

"Yahoo! is focused on making the world's daily habits inspiring and entertaining. And while we're starting with unique strengths, exceeding the growth that we aspire to will take multiple years. Essentially, we need to start a chain reaction. First, we need to achieve product excellence and differentiation by launching new revamped and innovative products. With great products, comes user growth and more engaged audiences. And finally, that user adoption drives advertiser attention, spend and, therefore, revenue."

"Focusing more on the pure advertising and monetization standpoint, there's greater opportunity with the big 4: Search, Display, Mobile and Video"CIT (CIT)

"Deposits are now almost $10 billion, representing over 30% of our total funding."Danaher (DHR)

"I think the competitive dynamics are increasing, as we've kind of talked about. There's the continued focus on loan growth in our competitors as well as ourselves, but we are being very, very disciplined and so we're going to keep that discipline."

On credit spreads: "So cash flow still is probably in the 500 (bps) range, plus or minus, depending on the transactions. Our ABL is probably more in the north of the 300. And then some of the ABL market, more of the retail flow stuff is probably in the 200 range. So at least for our core markets, we feel the risk return is still attractive"

"we have 10 (Boeing 787's) on order. Our first delivery is we have 2 being delivered -- or scheduled to be delivered in 2015. So I think -- from our perspective, I think it's a little premature to kind of sort (concessions from Boeing) out. But the viewpoint is that it's modest in our overall order book and we hope that these issues kind of get resolved because it's something -- the aircraft itself is something that is big in the industry."

"I was in China 2 weeks ago, and we spent a fair bit of time on this subject. I think it's interesting if you just look at our own trends through the course of last year, we really saw quite the bifurcation between our industrial businesses and our healthcare businesses, both LS&D and Dental. We were basically up 20% for the full year, and we saw that strength throughout the year on the healthcare side of the portfolio. We were down nearly double digit the first half on the industrial side...I think when we look at what's happened in Life Sciences & Diagnostics, we are clearly the beneficiary of a multi-year buildout with respect to the healthcare delivery, particularly in the West but also increased utilization."Seagate Technology (STX)

"For the December quarter, we shipped over 47 exabytes of storage with an average of approximately 823 gigabytes per drive. This reflects a 59% year-over-year exabyte growth, which is well over twice the current rate of areal density growth."

"Data consumption and creation, along with the increase of global internet connectivity continue to drive petabyte growth at rates that are significantly greater than the areal density growth rate."Illumina (ILMN)

"the Illumina Genome Network received orders for approximately 13,000 genomes. Today, interest in sequencing services remains high, including preliminary talks of large hospitals and governments that hope to sequence significant numbers of individuals."

"we've added significant new capacity to our San Diego facility and will open a new lab later this quarter in our Hayward location. This facility, along with improvements to our existing infrastructure, will provide the capacity to sequence approximately 30,000 genomes this year."EMC (EMC)

"We are squarely focused on several of the hottest areas in IT: cloud computing, big data and trust."

"the companies and entities out there understand that cloud and big data are going to change the landscape and if one doesn’t invest in these technologies, their companies will be left hopelessly behind."

How Long Does the Average Bull Market Rally Last?

As of today, the bull market which began in March of 2009 is 1,422 calendar days old. Over that whole period there have been nine drawdowns of greater than 5% which segment the bull market into ten periods of bull market rally.

The average bull market rally since 2009 has lasted 99 calendar days and has seen the market rise by 18.8%. By contrast our current rally, which started in mid November, is just 75 days old and has charted a 10.9% rise. If this rally were to last in line with the averages it would go on until February 22 and the S&P 500 would rise to 1608 before the next 5% pullback. Below is a chart of the full bull market broken down by periods of rally and >5% drawdown.

The average bull market rally since 2009 has lasted 99 calendar days and has seen the market rise by 18.8%. By contrast our current rally, which started in mid November, is just 75 days old and has charted a 10.9% rise. If this rally were to last in line with the averages it would go on until February 22 and the S&P 500 would rise to 1608 before the next 5% pullback. Below is a chart of the full bull market broken down by periods of rally and >5% drawdown.

Monday, January 28, 2013

Longest Interval Between Dow All Time Highs

Even though the Dow was down by 12 points today, it's beginning to look increasingly likely that we'll see a new all time high for the index in the not too distant future. The previous all time high was at 14,164, just 281 points away from where the index closed today. The index hit that mark in October 2007--a little over 5 years ago. That's the 5th longest span in history that the Dow Jones Industrial Average has gone without making a new high. After the depression it took 25 years to get back to its highest levels.

SPY vs. TLT

2013 is beginning the year with a strong dichotomy in asset class returns. While the S&P 500 is on pace to have its best January since 1997, the 10 year yield has moved higher by 20 bps. Expressed in more intuitive terms, SPY is up 5.3% year to date, while TLT is down 3%. The divergence between the two could represent some psychological pain for any investors substantially invested in bonds.

Friday, January 25, 2013

Offbeat Analysis: Optimum Class Size and Investing

An observation on the limits of cognitive capacity: the number of investments that any individual can properly monitor is not dissimilar to the number of children that an individual teacher can keep track of in a classroom.

It's logically accepted (albeit with some challenges to the conventional wisdom) that smaller class sizes are better for students because teachers can devote more time to each student. Similarly a smaller investment portfolio means that the investor can devote more time to monitoring each investment. There are tradeoffs though. Smaller classrooms mean a higher cost of education per student and smaller portfolios come at the expense of diversification.

Unfortunately there's no scientific way to determine the optimal level that balances these competing forces in classrooms or investments (sorry efficient markets theorists). However, qualitatively, the best size would be the largest size possible without sacrificing the individual attention needed to monitor the progress of each student/investment.

Looking at international data, the prevailing balance in the classroom seems to be in the 20 student range. In the average teacher's portfolio, each student is a 5% position.

It's logically accepted (albeit with some challenges to the conventional wisdom) that smaller class sizes are better for students because teachers can devote more time to each student. Similarly a smaller investment portfolio means that the investor can devote more time to monitoring each investment. There are tradeoffs though. Smaller classrooms mean a higher cost of education per student and smaller portfolios come at the expense of diversification.

Unfortunately there's no scientific way to determine the optimal level that balances these competing forces in classrooms or investments (sorry efficient markets theorists). However, qualitatively, the best size would be the largest size possible without sacrificing the individual attention needed to monitor the progress of each student/investment.

Looking at international data, the prevailing balance in the classroom seems to be in the 20 student range. In the average teacher's portfolio, each student is a 5% position.

|

| Source: OECD |

Earnings Call Notes 1.25.13

Like most analysts during earnings season I spend a lot of my day reading earnings calls. I've been trying to figure out a good way to incorporate some of the data that I gather from those calls into the blog. To that end below are quotes from calls that I've read today--snippets of information that I find relevant (typically on a macro/industry level) from companies that I have some working understanding of. Complete transcripts can be found at Seeking Alpha.

Raytheon (RTN)

Raytheon (RTN)

"Looking at the defense environment, the U.S. government averted the brunt of the fiscal cliff earlier this month. However, the ultimate outcome for sequestration was delayed and not resolved, and the new potential implementation date for sequestration is now March 1. The government continues to operate under a continuing resolution for fiscal year '13 that runs through March 27 or roughly halfway through its fiscal year."

"I would say that the department, State Department and the administration, understands that foreign military sales help us bridge the gap as we go through these headwinds in the sense that, if we have these programs in our factories, they help keep our overheads in control. They help, in some cases, to lower them, which allows the U.S. to make the decisions that need to be made."

On acquisitions: "Right now, I can tell you I've not seen a reduction in market prices. Everybody still thinks they're beachfront properties. And so for us, we're pretty disciplined here about how we go and do that. But as you look to the future here, people are going to have to evaluate what they have and maybe the prices will get better."Halliburton (HAL)

"North America, 2012 was a very challenging year for the industry. Operations we’re impacted by headwinds such as guar costs, pricing pressures and a significant drop in the natural gas rig activity. However I want to be clear before you listen to the rest of the presentation. We believe that the fourth quarter marked the bottom for U.S. land margins

we believe the rig count will continue to grow from current levels, but will average down slightly for the year compared to 2012."

"Many of our competitors are operating at breakeven or lost positions which should set a floor on stimulation pricing. However, an improvement in pricing will require a meaningful decrease in excess capacity"

"We are expecting the industry to add hardly any capacity this year and over time, we should see a drop in excess horsepower due to normal attrition. Increasing oil activity and rising service intensity will also help to a certain extent. However, we believe that without a significant uptick in natural gas drilling, it is difficult to see a path for pressure pumping equipment to reach equilibrium this year."

"Our view is that the U.S. natural gas drilling will not be a major activity driver in 2013, although the rig count in that area appears to have flattened. The decline in output from existing natural gas wells will likely be offset by additional volumes generated from new gas wells, the restart of shutting wells and associated gas from new oil wells if we see any meaningful uptick in gas activity that likely will not occur until the second half of the year. That being said, we still strongly believe in the long-term fundamentals of the gas business and are not going to abandon that market."

"Our growth strategy going forward remains the same. We'll continue to grow our market share in deepwater, in global unconventionals and in mature assets."

City National Bank (CYN)

AT&T (T)

Keycorp (KEY)"City National’s assets exceed $28 billion, a 21% increase as well from the prior year."

"Between September 30 and year end, we added a record $1.1 billion to City National’s loan portfolio."

"In the fourth quarter, loans really grew across the board."

"commercial line utilization increase for the second straight quarter topping 60% for the first time since the end of 2010."

"Particularly noteworthy improvement can again be seen in California’s housing market. The median home price in Southern California, for example, is up 20% year-over-year and home inventories are shrinking."

"I know how focused, almost all of you are on margin pressure and its impact on the industry in general. And there is no doubt that growing loans and deposits is putting more pressure on margin. But it does add to net interest income now, additionally when rates rise, these loans and deposits will provide large margin expansion for companies like ours."

"The flattening yield curve that took place during 2012 will no doubt make it harder for banks to grow earnings in 2013."

"I think one of the points that’s worth noting is that the average duration in our [securities] portfolio is relatively conservative. And we have deliberately tried to be conservative with it, just find the balance between getting a decent yield but not locking the company in to rates for the long-term that we would regret a few years out."East West Bank (EWBC)

"Year-to-date, return on common equity and return on assets were both above our peers at 12.3% and 1.3%, respectively."

"During the full year of 2012, East West grew non-covered commercial and trade finance loans by $1.1 billion or 35% to a record $4.2 billion"

"Provision for loan losses on non-covered loans was down 35%, net charge-offs on non-covered loans was down 62% from a year ago."

"Single-family loan originations...an average loan size of $389,000 and an average loan-to-value of 53%."

"many banks out there are offering 10-year fixed (interest rate swap) at a very low rate and I think that someday down the road, maybe 3 years, 4 years from now, I think they're going to be hurting in a big way."

"mostly in California and New York that we see activities in term of the commercial real estate."

"At this time, we would like to grow our loan portfolio across-the-board."Cash America (CSH)

"in 2010 and 2011...we mainly focused on C&I...But in addition to that now, we are kicking up our real estate origination for CRE and multifamily and so forth and even construction loans."

"In retrospect I think both our customers and our company have enjoyed the easy benefits of escalating gold prices for the past two years and now we need to recalibrate our training and marketing programs and store operating model to one that is more attuned to the emerging general merchandize product categories in disposition channels."

"you have a whole new emerging electronics categories with smartphones and tablets and a wide variety of other things we’re seeing in our stores today and we need to be training our folks to encourage our customers to bring in those items to the extent that they have those versus jewelry or scrap gold."

"I have got to believe that at this point that people are going to have to start using additional collateral to some extent that they offered up most of that excess gold and jewelry over the last few years"Kennametal (KMT)

"Political and economic uncertainties led to spending deferrals and inventory destocking by customers. Those conditions resulted in a weaker-than-expected global investor production across certain end markets and geographies."

"In addition, our sales were unfavorably impacted as a number of customers who extended shutdowns year end holidays. This trend was more severe in Europe but it occurred in North America as well."

"We now expect fiscal '13 sales to be between negative 2% and negative 4% with organic sales ranging from negative 7% to negative 9%."

"we have seen an uptick in Asia. However, it's still, year-over-year, a negative growth"Jacobs Engineering (JEC)

"Oil and gas market remains very, very strong. It's one of our hottest markets."

"And in the chemicals market, it's as good as it's ever been in my memory. It's a very strong market for us right now. It's obviously a business where there's a key driver is this cheap gas"

Question from an analyst: "one of your peers, couple of weeks ago, came out and said that labor constraints were looking like it was becoming a slight bit of an issue sort of in the Gulf Coast area on the petrochem side. So I was just wondering if you can -- it's the first time I've sort of heard that in a while. "

Response: "we will continue to see pressure on escalation and rates, but it's all good news. The craft side of the business is probably another 8 months to a year away before we start seeing pressure there, but on the engineering side, we're in the throes of it right now."

"my concern about the fiscal cliff discussion for a while was that it might push all these projects significantly out. And it doesn't seem to have done that. So our customers seem to be planning their investments, particularly ones in the natural gas or in the chemical side,"

Comment from analyst: "So it sounds like some of your labor costs are starting to move up in the market, starting to tighten"Microsoft (MSFT)

"Windows 8 is a sort of big, bold, re-imagining of Windows across the whole ecosystem, and I think this was the start of that process. I think, we all collectively learned a lot about from the user interface to the touch devices. And, as I tried to give context on the call, there's a lot of things we are working on with our partners that I think to continue to drive this process forward over the next several quarters whether it's the chipset, whether it's with developers or the kinds of applications that people want and certainly for the kinds of touch devices that they write price points that consumers want I think all of that continuously improving, we are continuously learning and happens over time, but this is a big ambitious re-imagining of Windows, and this quarter was the first step in that process."Starbucks (SBUX)

"a Starbucks card was perhaps the nation’s single most frequently given holiday gift, with one in 10 U.S. adults receiving a Starbucks card"

"The U.S. remains a market rife with growth opportunity for Starbucks, and we will profitability capitalize on this opportunity by adding 1,500 new stores in the U.S."

"Starbucks’ China and Asia-Pacific segment now spans 12 countries that by the end of fiscal 2013 will grow to nearly 4,000 stores, including 1,000 stores in Japan and 500 in Korea."

"We had 86% more customers sign up for a My Starbucks Rewards card in the first quarter of 2013 than in the first quarter of 2012. And it’s not that these new card customers didn’t know where to find us last year. It’s that we are more deeply connected, and even more relevant, to them than any other time in our history."Procter and Gamble (PG)

"[plan] further reduction of non-manufacturing [headcount] by additional 2% to 4% per year from fiscal year 2014 through 2016."

"there are new categories we have entered too. Jon mentioned the ZzzQuil in sleep aids. We entered the auto care fragrance category. And as we also talked, we have bolstered our new category innovation as well and we fully expect some of those innovations to come to market over the next year or so."

"we are growing or holding share in the 60% of our business in the U.S"

AT&T (T)

"we believe we are going change every aspect of our customers lives. How they buy things. How they manage and secure their homes. How they access entertainment. Their experience behind the car wheel is going to change. There is going to be a whole healthcare ecosystem change. And I can go on, but it’s clear that the industry is moving beyond the device and into a new era of solutions and services. "

"the question you have to ask is are there opportunities for us to participate in that growth outside the U.S."

"Our average C&I loans were up 21% over last year and led our year-over-year loan growth."

"we will maintain a moderate risk profile"

"Our capital remains a competitive advantage for us in both the intermediate and long term."ITT Education (ESI)

"prospective students are more sensitive of the cost of postsecondary education and are making educational decisions based on their perceived opportunity to derive value from their educational investment."AmerisourceBergen (ABC)

"demographic trends and health care reform initiatives will expand coverage to the uninsured and should drive organic growth in our industry over the next several years"Southwest Airlines (LUV)

"We are seeing encouraging signs in our business travel trends."United Continental Holdings (UAL)

"We did not achieve our return on invested capital target in 2012 and we’re absolutely not satisfied with the financial results we produced last year."

"look the [787] is a terrific aircraft and customer loves the airplane and I have no doubt the customers will flock back to that airplane as soon as we get it back up again."Avnet (AVT)

"After several quarters of a somewhat cautious technology spending environment, certain segments of our served markets demonstrated relatively better strength in the December quarter."Flextronics (FLEX)

"the macroeconomic environment remains very soft for electronics hardware. The semiconductor industry association, or SIA, forecast for the start of 2012 was for 7.6% growth. The semiconductor industry ended the year with a negative growth rate of about 3.2%. These numbers would have been lower if not had been for the strong growth and volume from both Samsung and Apple."

"we also announced an important multibillion partnership with Google-Motorola Mobility to streamline their supply chain operations and position Flextronics as a key supply chain partner for current and future hardware products within its ecosystem"Synaptics (SYNA)

"The latest projection from IHS Research in November shows the smartphone market hitting 660 million units in 2012."

"IDT’s projections for notebooks with touch is now 25% of the unit shipments by 2014."Silicon Valley Bank (SIVB)

"For the full year 2012, we grew average loans by $1.7 billion or 30%"

"Yeah, we see more people entering the market [for loans to venture stage companies]. And I guess it's not surprising, mainly because it's one market. And we've said this for years, and we should expect to see this, that it's a high-growth market, it's performed well through multiple cycles, and again, it's one of the only fast-growth areas in the market. So that's not surprising...So, yes, we have acknowledged that City National has been hiring in the marketplace and they will compete with us."Xerox (XRX)

"Xerox is a company that is going through a seismic transformation."

"The shorter contract and less megadeals is a sign of the times today. We had significant pressure in both government and large enterprises, given a very weak macroeconomic environment."LG Display (LPL)

"We expect the continued risk demand trend in 2013. However, the industry supply increase would be also marginal this year."

"several companies will execute fab conversions in second half, which would have a positive impact on the supply side."

Thursday, January 24, 2013

Earnings Call Notes 1.24.13

Like most analysts during earnings season I spend a lot of my day reading earnings calls. I've been trying to figure out a good way to incorporate some of the data that I gather from those calls into the blog. To that end below are quotes from calls that I've read today--snippets of information that I find relevant (typically on a macro/industry level) from companies that I have some working understanding of. All the transcripts are found at Seeking Alpha.

Raymond James--RJF (Regional Broker)

Raymond James--RJF (Regional Broker)

"assets under management, have gravitated more towards fixed-income and our retail clients have gravitated more to fixed income as in asset allocation. So with all those factors at play, we're not as sensitive to the U.S. equity markets as we have been in the past."

"I think that our investors' sentiment and our sentiment -- investor sentiment survey is up. We haven't seen a massive move to equities. I know a lot of the funds are showing big inflows. I think we've been more with our investors, we try to keep them engaged, maybe they've been a little more engaged in other places. So I haven't seen a big movement yet. But having said that, the commission levels in January have been pretty good so far. I'm a little bit behind in terms probably up to today. But I mean, I can't say we've seen a huge flood into equity since the beginning of the year. "McCormic--MKC (Spices)

"Globally, digital marketing was 12% of our total spending, up from 5% in 2010."

"Our brand marketing plans include further increases in digital marketing, support for new product launches and a sharp focus on retail price points. "

"Sandy. While this devastating storm had a limited impact on our sales to customers in the Northeast, it did impact a number of suppliers in this area, which created product shortages during our critical holiday selling period. We also lost several ships of production time in our manufacturing distribution facilities in Maryland."

"we've had about a 45% increase in commodity cost over the last 4 years and have taken about 25% pricing and we've taken a number of different actions along the way, and we are always evaluating the impact of that on volume….and by the way, what we have seen as our pricing has gone up, we have seen those price gaps close now as competition, largely private label, has also taken place increases to either catch up or improve their margins."

"About quick service restaurants: I'm following our customers' releases as closely as -- probably closer than you are because they really impact us. But I would say that we think that it's going to be fairly challenged."

"[around the holidays] typically we do see an increase in branded shares for a couple of reasons. One is consumers are less willing to take chances on their meals."Logitech--LOGI (Consumer Electronics/Peripherals)

"As we discussed in our Q2 earnings call the main factor in our weak performance was a significant weakness in the global market for new PCs. This weakness which had a negative impact on sales in all our PC related categories reflects the combination of the slow transition to Windows 8 and the growing popularity of tablets and smartphones as mobile computing devices."Hill Rom--HRC (Healthcare, Hospital Beds)

"Our rental business in North America remains challenging due to continued efforts by hospitals to reduce their operating and supply chain costs. We expect this to continue given the economic pressures they are dealing with. "Nokia--NOK (Cell Phones)

"we shipped 6.6 million Smart Devices units of which 4.4 million were Lumia devices."

"Now more than ever, operators are pushing for a third ecosystem to emerge, and they are committing to more marketing, more training, and more in-store displays to help Windows Phone and Lumia to grow."Grainger--GWW (General Business Supplies Distribution)

"Light Manufacturing was up in the high-single digits; Heavy Manufacturing and Commercial were up in the mid-single digits; Government and Retail were up in the low-single digits; Reseller was flat; Contractor was down in the low-single digits; and Natural Resources was down in the mid-single digits."Symantec--SYMC (Cyber security. Lots of interesting discussion. Worth doing a full read through)

"welcome to the unveiling of Symantec 4.0"

"despite the fact that we have such great point solutions built mostly from acquisition…We haven't really integrated the value of these different point solutions"

"the porous nature by which information is flowing across enterprise, individuals, governments and your personal world. Those boundaries are now taken down."

"There was one large pharmaceutical company, and as the CIO was describing his real estate he said, look, we have 60,000 PCs. We have about 7,000 Macs. We have 15,000 iPads and over 10,000 Android smartphones in their environment that he was aware of. And he said what he needs is an offering that allows him to let people use those devices but, at the same time, protect the business. "

"while we had the great assets, we didn't have a strategy or an operational plan to focus on delivering value for customers, and that's what Symantec 4.0 is all about."Western Digital--WDC (Hard Drives)

"there are early indications of consumers' stronger intentions to purchase new PCs this year."

"The HDD market shipped approximately 136 million units during the December quarter, slightly less than the 140 million units we anticipated in our guidance."Apple--AAPL (Fruit company?)

"Apple is in one of the most prolific periods of innovation of new products in its history."

"We have now sold well over 0.5 billion iOS devices"