Credit Quality

Over the past several quarters, credit has been healing at banks. Specifically, noncurrent loans have been falling, albeit slowly from peaks.

|

| Click to Enlarge (all charts) |

Using the 80s as a barometer, it could be a significant amount of time until bank balance sheets are fully healed. Elevated noncurrent assets remained on bank balance sheets for 10 years between 1984-1994. Also there were a number of false starts where credit looked to be healing and noncurrent loans went on to increase. Hopefully we're not entering a similar environment.

Not surprisingly, in this cycle the the most persistent noncurrent asset class is residential real estate.

Residential loans have increased as a percentage of noncurrent loans, even as the dollar value of residential noncurrent loans has fallen. This indicates that noncurrent residential loans are being resolved at a much slower pace than other types of loans.

Still, overall charge-offs and provisioning continues to move in the right direction. In anticipation of slowing credit deterioration, charge-offs have exceeded provisioning for the last 6 quarters.

Capital/Liquidity

From the perspective of capital, the banking system continues to show improvement as well. Capital ratios are above pre-crisis levels both on a leverage and risk weighted basis.

From a historical perspective, capital at US banks has been increasing for many years and is at high levels today. The leverage ratio is one of the more strict measures of bank capitalization. The current level, above 8% for our largest banking institutions, indicates an increased ability to weather a double dip.

Aside from pure leverage, the banking system has significantly reduced the "riskiness" of its aggregate portfolio down to 1993 levels. While the adequacy of risk weightings are debatable, in general balance sheets are likely more resilient to a weak economy.

Profitability

One of the more prominent areas of concern for equity investors has been the long term profitability of banks due to 1) a low interest rate environment and 2) more strict capital requirements. While these problems could manifest in future economic cycles, for now banks appear to be repairing profitability reasonably well. Return on assets was 0.85% annualized for 2Q11. This is pretty healthy considering that banks continue to have elevated costs related to credit.

Looking at the affect of the low interest rate environment, NIM across the banking sector has trended somewhat lower over the past decade; however, US banks' NIM is still robust compared to many other international banks.

Isolating for the effect of leverage, profitability looks a little more constrained on an ROE basis. In 2Q11, industry ROE was 7.5%--well below prior peaks.

Growth

Another area of concern for banking stocks has been loan growth, which appeared for the first time in 11 quarters in the 2Q11 (1Q10 loan growth resulted from a reclassification of off-balance sheet loans to on balance sheet).

In a positive sign for the economy, a major driver of the loan growth came from commercial customers.

In addition to new net borrowing, commercial customers increased utilization of credit lines, which had been relatively low on a historical basis.

Looking at the other side of the balance sheet, deposit growth continues to be extremely strong for banks. Today, banks' loan to deposit ratio sits at multi-decade lows. A large deposit cushion gives banks more flexibility in terms of liquidity in the event of a banking panic similar to 2008.

Longer-term trends

From a longer-term perspective, there are some interesting trends which have materialized in the banking sector over the last couple decades, some in relation to the credit crisis and some which may be altered because of it.

One area significantly affected by the housing bubble has been the availability of construction loans. As the chart below demonstrates, there are a couple-thousand fewer institutions putting significant amounts of capital up for construction loans than there were in 2007. Construction loans had the highest loss severity and delinquency in the crisis of any type of loan. As a result, it may be a long time before these come back.

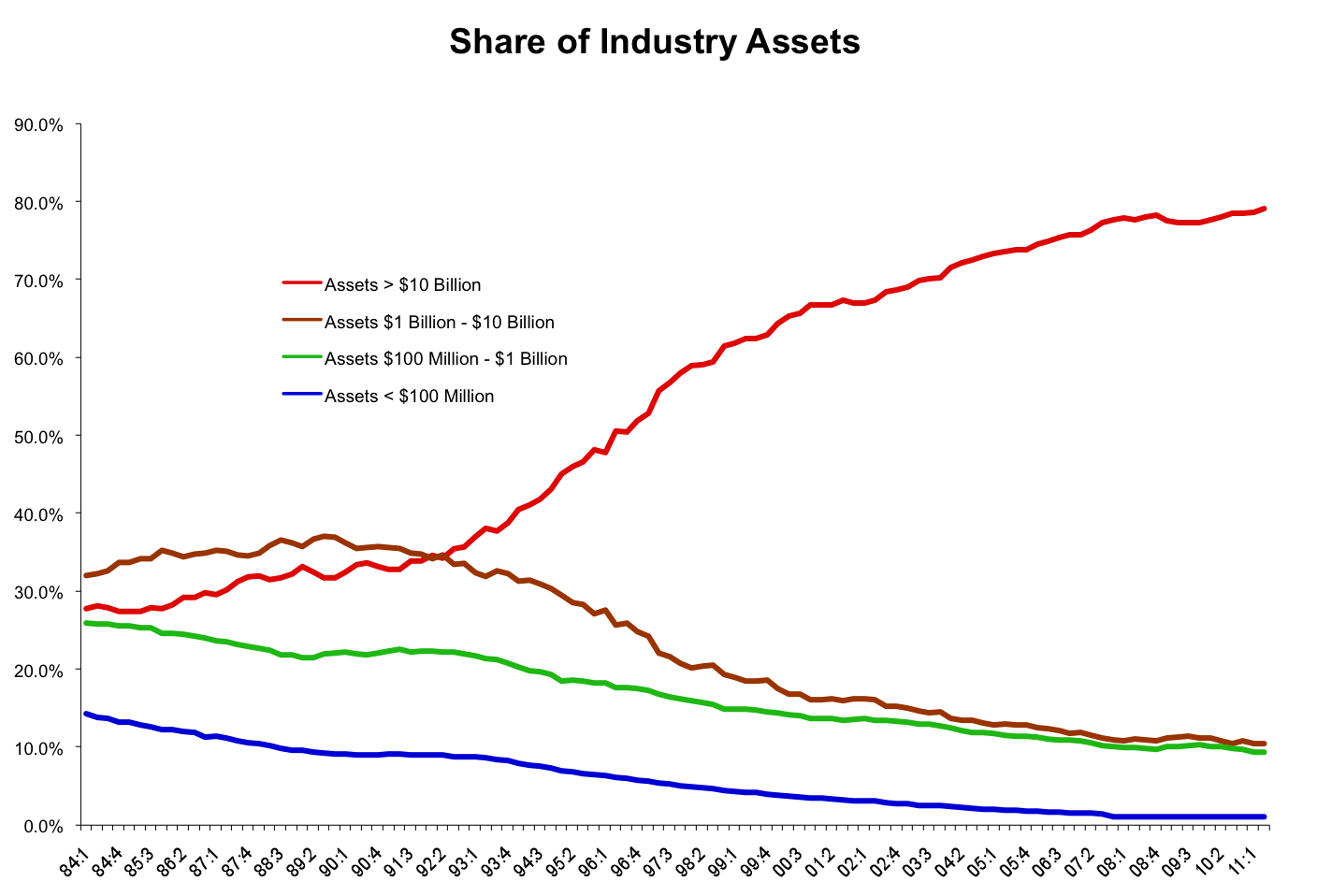

Another longer term trend has been increasing consolidation in the banking system. Most other nations do not have the same fragmentation that the US banking system does. Since 1995, the number of banking institutions has fallen significantly, but it still remains highly fragmented.

As a result of Basel III and Dodd Frank, the competitiveness of these larger banks has been called into question. For investors with a longer term outlook, a fundamental question should be whether new regulation will reverse this trend of consolidation. If it doesn't, then a rehabilitated banking system and depressed prices could be the right ingredients for an M&A wave.

No comments:

Post a Comment

For compliance reasons, I don't post comments to the site, but I do like hearing from readers and am happy to answer any questions. Feel free to use the comment box to get in touch. Please leave an email address in your comment so that I can write back, or email me directly at Skrisiloff@avondaleam.com.