The indicator was developed by two professors, Marcelle Chauvet and Jeremy Piger. The inputs are: "a dynamic-factor markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales."

I'm not particularly familiar with this indicator so it's tough to know what the biases could be, but I generally tend to be somewhat skeptical of models like this one.

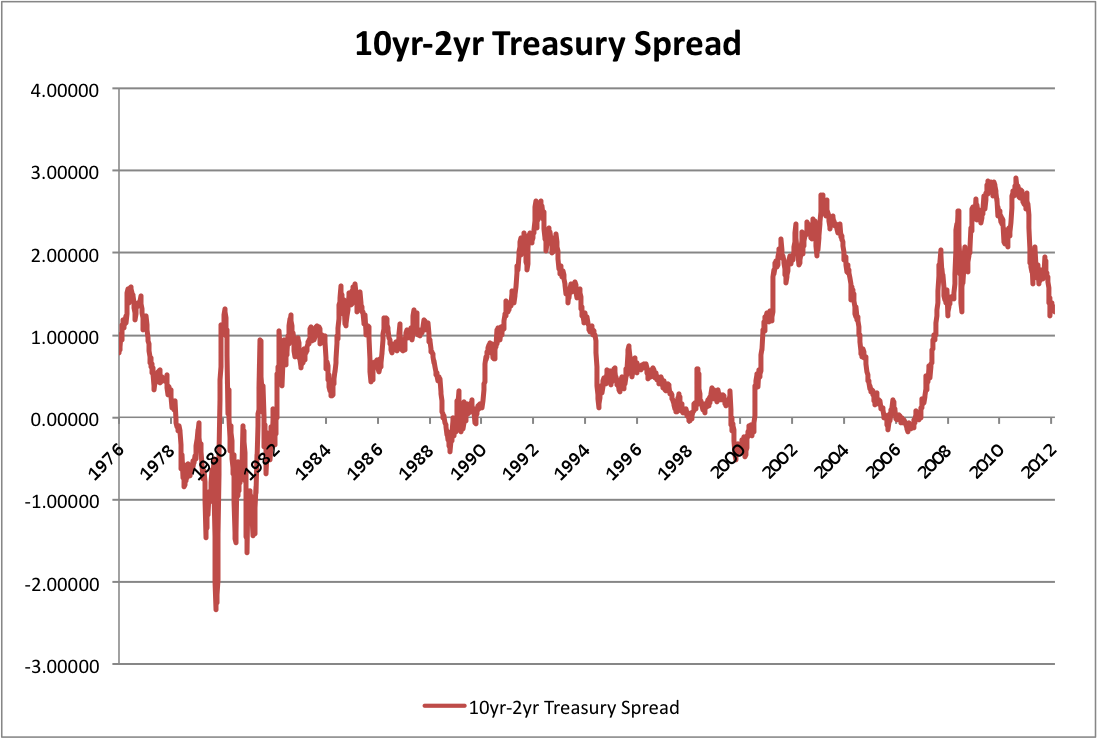

A more time tested recession indicator is the slope of the yield curve--when the spread between 2 year and 10 year treasuries is inverted recession normally follows. In a zero interest rate environment the yield curve may have lost some of its informational content, but it's been a great cyclical indicator for a long time and it's grounded in sound economic logic, so it shouldn't be totally ignored. Today, even though the curve has flattened since '09 it is still not at or near the zero threshold. As of right now I'm still on the lookout for the yield curve to go completely flat or invert when recession is imminent, even in this environment.

A more time tested recession indicator is the slope of the yield curve--when the spread between 2 year and 10 year treasuries is inverted recession normally follows. In a zero interest rate environment the yield curve may have lost some of its informational content, but it's been a great cyclical indicator for a long time and it's grounded in sound economic logic, so it shouldn't be totally ignored. Today, even though the curve has flattened since '09 it is still not at or near the zero threshold. As of right now I'm still on the lookout for the yield curve to go completely flat or invert when recession is imminent, even in this environment.

To clarify, I did write yesterday in my investor letter that I think recession will happen sometime in the next presidential term, but that doesn't necessarily mean it's imminent. My base case is that it could start sometime late next year absent a totally botched fiscal cliff. The forecast is mostly reliant on the average duration of economic expansions. As I've written before, this expansion would be short even compared to the 1933 expansion if it ended today.