Banco Santander (SAN)

capital ratios rising for the sixth year running up to 10.33%. loan-to-deposit ratio is now below 100%Southern Company (SO)

we have assigned since the beginning of the crisis over EUR 23 billion to specific provisions for loan losses and real estate, which account for 10% of our total loan portfolio in Spain.

As for our NPL ratios, the group ratio was 4.54%

And if we look at lending, lending fell overall by 6%, but big differences between segments. real estate purpose fell 32%; the individual household mortgages and consumer loans down 7% due to household deleveraging...reasonably stable lending to companies and to the public sector...balances with large corporates have fallen, too...because of continued deleveraging by corporates.

Brazil, the macroeconomic environment has been quite different to what we expected and what the market expected...Growth on GDP was of about 1%....we think that is going to pick up in 2013 and grow at about 3%. Interest rate at historic growth, 7.25% and inflation almost 6%.

In Spain, the recapitalization of banks and the private sector adjustment already completed

In short, we believe that the worst part of the cycle is already over. Realistic exposure is fully provisioned.

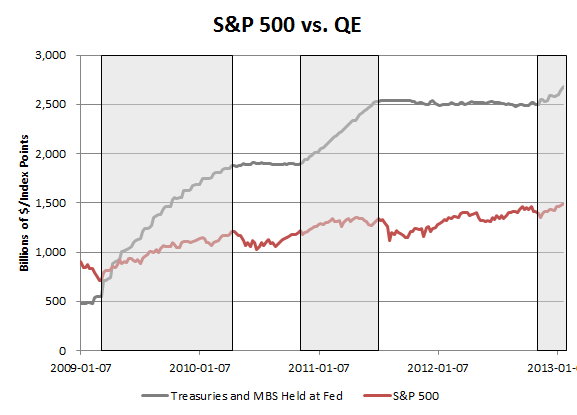

Whether we plan to repay anymore or return anymore [of the LTRO], we are using as cushion basically or insurance...So the decision of whether to repay any more or return any more, well, the answer would be probably, yes. But it will depend on the evolution of the markets and the impact on our income statement, well, it costs 75 basis points...And the liquidity buffer had a negative impact on our income statement

We continued the ongoing transformation in our generation mix, generating more energy from natural gas than coal for the first time in our historyDow Chemical (DOW)

our kind of color on where we believe the economy is headed is slightly more bullish than we were, say, in the third quarter. We are expecting a backend loaded economic recovery but I feel pretty good about it right now based on what we see.

energy efficiency has almost no influence on the consumption of our customers. 88% or so of usage can be explained by either the income growth of our customers, the price of our product and weather.

We all have these goofy devices. We all have iPads and iPhones and bigger plasma TVs and everything else and when we see the progression that people are moving from small homes to apartments into you now primary housing, we see a growth in square footage per person...All of these things contribute to usage growth

if the final rule is anything like the proposed rule, conventional coal generation is just not doable...I go back to the families we serve, 48% of which make 40,000 or less, those folks make tough kitchen-table economic decisions every day. Their demand for energy is relatively inelastic, and so anything the EPA does which adds cost to energy tends to slow down our economic recovery

wet shale gas dynamics are fundamentally changing the game for integrated North American based producers like Dow. This is clearly evidenced by operating rates in the United States and Canada being in the 90s, while Asia and Europe have been in the 70s.Time Warner Cable (TWC)

as global demand outstrips supply in the next few years and world GDP gains further traction, we anticipate operating rates higher than 90% leading to substantial margin expansion, a double peak, so to speak.

Dow's feedstock flexibility will allow us to continue to pivot so that we continue to take advantage of our uniquely advantaged feedstock slate and we are building on this advantage.

Our programming costs per subscriber has grown 32% in the last 4 yearsQualcomm (QCOM)

Our residential video ARPU increased 16% over that same period, so we've effectively raised pricing a little faster than inflation but only half as fast as programming costs have risen.

ARPU per customer relationship, which increased 4% over last year and is approaching $120 per month

We do not pretend that these deals [i.e. the Dodger's deal] are inexpensive or cheap. And our sense is that if we're going to carry these games, they're going to be expensive when we get them. So what we think we've done with these deals is to minimize and stabilize the cost over a long time period.

On Google in Kansas City: The reality is, today, there are not really applications that require 1 gigabit per second.

this brings 3G penetration to 29% in China, so excellent progress and still plenty of opportunity aheadUPS (UPS)

our design pipeline continues to grow. There have been more than 600 Snapdragon-based devices announced and another 170 plus devices announced based on our Qualcomm Reference Design solutions.

we are seeing more efficiency in the 3G, 4G inventory channel as the industry continued to move toward an open retail channel versus a carrier centric channel

We are reaffirming our estimate for calendar 2013 3G, 4G device shipments of between 1 billion and 1.07 billion units, up approximately 8% to 15% year-over-year

in the U.S, we were off to a surprisingly strong start in January

Holiday retail sales came in slightly below expectations but UPS still hit a new high, delivering over 500 million packages globally during peak season.

On our peak air day, Christmas eve, UPS delivered over 8 million air packages, more than 2.5 times our normal air volume and over 1 million pieces more than last year.

UPS annual revenue of $54.1 billion was our highest ever, as were the 4.1 billion packages we delivered globally.

I think that overall we still see 2013 as a slow growth economy.

Facebook (FB)

We started off the year with no ads at all on mobile and we ended up with approximately 23% of our ads revenue coming from mobile in the fourth quarter.Paccar (PCAR)

Marketers are realizing more and more that Facebook is one of the best places to reach their customers on mobile because of our unique ability to reach specific target audiences at scale.

our total expenses, excluding stock comp, will likely grow by somewhere around 50% in 2013

PACCAR's retail share of the U.S. and Canadian Class 8 truck market was 28.9% and DAF's share of the European above 16-tonne market was 16%Core Labs (CLB)

Looking at the truck market overall in 2013. The U.S. and Canadian Class 8 industry retail sales are estimated to be in the range of 210,000 to 240,000 units. In Europe, the "greater than 16 tonne" truck market is anticipated to be in the range of 210,000 to 250,000 units.

Natural gas will be a factor, but at this time it's a pretty small factor. We'll just have to see over time how the infrastructure shakes out

Yeah, Jeff, we actually don't think that the shale plays are well understood at this point. Just over the last couple of quarters, we have been able to determine through our fracture diagnostics technology that additional stages, closer spaced, so you have more in greater contact with the reservoir phase is going to proliferate more stages and more closely space stages.

We believe that currently there are only one or two countries that have spare capacity and that amount is fairly limited. If we get some robust economic growth around the world, we are going to see crude prices, Brent prices right back at $150.

Q: perhaps two substantial liquids discoveries yet to be made or announced in North America, can you give us a feel for when we might, the mystery might go way? A: Well, that’s up to our clients, acreage positions are being taken and I got a fairly, once of the acreage positions are established as which happened in the Eagle Ford and then in the Utica announcements will be made. So it’s not up to us, its up to our clients.

Conoco Phillips (COP)

Viacom (VIA)We ended 2012 with just over 8.6 billion BOE of reserves, up 3% overall compared to 2011. Importantly, we added 942 million net BOE of reserves organically resulting in an organic reserve replacement rate of 156%

I think as we look out and think about the future opportunity, I think with this unconventional revolution that we are seeing in North America right now, and some of the technology advances in the deepwater arenas that are becoming pretty perspective. It’s kind of in my view turn from a bid of resource scarcity that was leading to a lot of merger synergies over the last 10 or 12 years and resource capture into a view now...we just think that growing organically, there is the opportunity set to go do that and the option value associated with growing organically is, we thought better in our portfolio then trying to do that through an M&A channel, or some resource access that way.

the consistent refrain we hear from our audiences is that they want new shows and new episodes in faster cycles, and so we are delivering at all our networks, accelerating development timelines and production to accelerate our ratings turnaround.Under Armour (UA)

original programming that’s new and exclusive to us where we own all the rights and we think that is going to be critical as you move into the future where this program lives across platforms and around the world.

we have content on platforms like Netflix and Google. The growth of streams of our content far outpaces the growth of subscribers that they have

In our IPO year of 2005, compression represented 64% of our apparel mix. This past year, that compression number was down to just 14%.Cullen/Frost Bankers (CFR)

we want to go back to this concept around cluster marketing, and the idea there is to create holidays. So holidays are places where based on the entire brand meets at once. What we want to do is consolidate our spend to tighter, but louder messaging

For the year, return on average assets and equity were 1.14% and 10.03%...average total deposits were $17.3 billion, up 13.6%...average loans were up 11.2%Bank of Hawaii (BOH)

It’s really nice when you’re growing this strong organically. Just to put it in perspective, the biggest bank we ever bought was about a $1 billion. And today, we’re growing at a rate of about $2 billion a year. So this organic is getting better.

You don’t just go make the first call and get the loan...We know that the work we do today is going to payoff about a 120 days from now.

you’ll see a juvenile delinquent come in [to our markets] every now and then, and that juvenile delinquent doesn’t mean a little bank. It means, usually the too-big-to-fail will come flying in with some crazy pricing.

We had a record number of visitors to Hawaii this year and visitor spending reached a record-high of 14.3 billion that's up over 18% for the year. most of that increase coming from our International segment.

Year-to-date return on assets was 1.22% and return on equity was 16.2%. Our year-to-date efficacy ratio was 57.9%, a reduction from 59.2% in 2011. Earnings per share was up 8.3% in 2012. Loans grew 5.7%. Shareholders equity grew 1.9%.Callaway (ELY)

From a market share basis, through November our US hard goods market share declined to 14.4% versus 15.6% in 2011Hershey (HSY)

what’s occurred between 2007/2008 and the current somewhat compressed gross margins is rising costs out of Asia where we source most of our products, and an increase in the amount of technology in the products such as adjustable drivers and other technologies that in many instances are being sold at the same price points that we’re popular in the market in 2007/2008. So those factors are real in our industry as candidly they are in all industries, and we have to work through those.

Halloween results were in line with expectations. The late October storm that affected the East Coast did not have a material impact on our overall Halloween results.